10 ‘Suggestions’ of FI (for Newbies to Financial Independence)

Many years ago I was driving home from a bachelorette party in Georgia with one of my sweet friends from undergrad, Kara. We were in the bygone phase of the internet when everything was a top 10 listicle or a personality quiz somehow related to whatever was popular at the moment. I remember being personally enthralled with anything related to Harry Potter (still true) and so couldn’t wait to find out which Hogwarts house I belonged to (Ravenclaw) or what form my Patronus would take (can’t remember but let’s call it a Maya-shaped pup).

We were joking about how there was a quiz for literally anything, and so I asked Kara to find one to see what kind of burrito we would be. Sadly, I can’t remember our results. Surely it was highly scientific, and the type of burrito was spot on.

What I do remember is her burst of laughter (she has the BEST laugh) at finding out that a burrito quiz did in fact exist, and also that it was a sunny, beautiful drive. Maybe retirement should include more road trips with girlfriends. Noted.

In this blog post we are going to revive the long lost art of the listicle- but with a purpose! (My apologies if you were hoping for a burrito quiz.) If you are new to the Financial Independence, Retire Early (FIRE) movement, call this your starting place. You’ll be introduced to some of the main concepts and voices in the space, all nicely linked so you can begin your deep dive down the rabbit hole like so many before you.

Also, this post is titled the “10 Suggestions of FI” instead of the ‘commandments’ or ‘mandates’ because nobody needs that kind of energy in this, the year of our lord 2026. Feel free, as always, to take what works for you and leave the rest.

Suggestion 1: Spend less than you earn, invest the rest (in a low-cost index fund)

-Everyone, but really JL Collins

If you only bookmark one suggestion from this whole list, this is the one. When you spend less than you earn and invest the rest in a low-cost index fund (the FIRE community is in a semi-monogamous relationship with VTSAX at Vanguard) you will become wealthy. Just how quickly that happens depends on how much you invest, (see suggestion #5) but it will happen.

Action Step: It’s your lucky day- you get two action steps for the price of one from the jump!

Option 1: purchase JL Collins’ book if you wish to understand this principle even slightly more before you get started investing. I promise that it isn’t boring and even the author will encourage you to only read what is applicable to your situation. This book is the FI bible.

Option 2: do a google search for “best low-cost index fund that mirrors the S&P 500.” Choose one at Vanguard, Fidelity or Schwab. Open an account at said firm and create an automatic, monthly investment for the amount of your choosing. The amount doesn’t matter as much as simply getting this investing muscle going. You can increase it later.

Suggestion 2: “You can afford anything, but not everything…” -Paula Pant, Afford Anything

Paula Pant is my favorite financial podcast host for oh so many reasons. She’s as smart as h-e-double hockey sticks, an amazing interviewer, and she starts every podcast episode with the quote above. She goes on to say that every resource that matters in our personal lives is finite- our time, our money, etc. Choosing one thing necessarily means not choosing something else.

This can really be applied to anything, but we’re talking money here so this one is for the folks who like to spend: if I asked you what your values are, what would you say? Taking it a step further, would your spending match your values?

For example- if you told me that your values are spending time with family, healthy eating and travel, would I see evidence of spending in those areas on your most recent credit card statement? Or might there be $500 in Door Dash spending and 15 different streaming subscriptions?

This is NOT to shame anyone (I’m not looking at your spending anyway so what do I know?) but I do think it is a helpful gut check, and maybe even an opportunity to start living your values more fully through intentional spending.

Action Step: Write down your top 3-4 values. If that is too esoteric, try thinking about it in terms of what you love doing or spending money on. Then, print out the last 3 months of credit and debit card statements. Highlight every time a purchase was directly related to one of your values. What do you notice?

Suggestion 3: “Spend extravagantly on the things you love, and cut costs mercilessly on the things you don't.” -Ramit Sethi, Money for Couples

Whoa! Look how related this is to #2!

Ok. So if you completed the action step from Suggestion #2, you should have a very clear picture of exactly where your money is going. Is it going towards things that you love? Or is it going towards things that you can’t remember or don’t care about?

Ramit Sethi calls the “things we love to spend money on” our money dials. My money dials are time freedom, health, travel, and time spent with family & friends.

If you were to peep into our credit card statements for the past few months, you’d see evidence of the following:

Time freedom: 50% of our income going to savings and investing, so that we can retire early.

Health: high grocery bills (we cook almost all of our meals and they are high in protein + veg), a subscription for Ryan for indoor cycling workouts, therapy bills and a subscription to TBM for inner child healing for me.

Travel: This one doesn’t pop up every month, but I just booked all of our post-retirement stays for July-December. Woot!

Time Spent with Family & Friends: Ryan just took his daughter on a snowboarding trip to MT, and we spend freely on nights out with friends (including a magic show!)

What you won’t see on our credit card bills is just as important. Because we don’t care about these things, you won’t see manicures (or anything that falls under what Katie Gatti Tassin calls the ‘hot girl hamster wheel’ and I call ‘aspirational beauty products’); high clothing expenses (our average is less than $100/mo); car payments; fast food/food delivery; anything from Target; etc.

My not having these expenses doesn’t mean I judge people who do- it simply means that what we care about is different. That’s normal- we are all different people, right?

Action Step: If you haven’t done the action step from Suggestion 2, now’s the time.

Suggestion 4: FI is better with friends. -Brad Barrett, Choose FI

Did Brad really say this first? I’m not entirely sure. But he & his co-host, Jonathan, have built a community of folks worldwide who love hanging out with each other.

To be honest, pursuing financial independence can be a bit lonely sometimes. Not many people talk about money- but when you are going after something big and audacious like early retirement, you want to talk about it!

Ryan & I have gotten so much out of attending our local ChooseFI meetups every month here in Charlotte. It’s truly one of the things I’ll miss most when we retire and start to slow travel- but we hope to join in with other local groups as we go.

Action Step: Click here to see where your nearest local group is meeting- then mark your calendars and join in. I promise you, you’ll be welcomed with open arms.

Suggestion 5: If you know your savings rate, you know how many years it will be until you can retire. -Mr. Money Mustache

This is where the rubber meets the road, where you take your power back, where things get real. There’s no need to expound here, because MMM wrote the most referenced article in all of FI-dom about this topic, and it’s linked here.

Action Step: Read it, baby!

Suggestion 6: Your FI number = your yearly spending x 25 -Bill Bengen, the Trinity Study

Ok. First I need to say that I did not link the actual Trinity Study above because that would be yawn-city. In it’s place, you’ll find a podcast episode where Bill is interviewed (by Paula Pant, who else) where he discusses the study and it’s implications for early retirees.

Finding out your FI number is the first step for many FI folks, and it provides a handy goal post to work towards. There is a lot of nuance, as with any broad based “rule” that applies to the masses, but for our purposes in FI newbie-land it’s the perfect starting point.

Your FI number is your annual spending multiplied by 25. So, if your annual spending is $60,000 (because you’ve analyzed your spending and are only spending on what truly matters!), then your FI number is $60,000 x 25 = $1.5 million.

This means you’d need $1.5 M saved, invested, and in upcoming Social Security (or pension, or inheritance, or whatever) to retire.

Action Step: Calculate your yearly spending. An easy way to do so (at least at first) is to take the average of your last 3 months of expenses and multiply them by 12. Keep in mind, there is almost always an opportunity to cut out spending that doesn’t matter as much.

Suggestion 7: “The key is remembering that anything you buy and don’t use, anything you throw away, anything you consume and don’t enjoy is money down the drain, wasting your life energy and wasting the finite resources of the planet.”

-Vicki Robin, Your Money or Your Life

Leave it to Vicki to keep it real. The key here is intentionality. Does this thing you are purchasing have multiple uses and/or give you joy? Does it relate to one of the money dials you discovered above?

Or- and again, no shame in this- are you buying this thing because an influencer convinced you to, or because your neighbor has one, or because you’re bored?

We can’t be perfect about this, friends. But we can be 1% (maybe 10%? maybe 25%?) better. I’ve started thinking about the lifespan of things that I purchase. How long until this thing ends up in the landfill, as it is destined to be someday? What resources did it take to create this thing? Is it possible to know if any person, animal, or natural resource was harmed in the making of it? And if so, can I make a different choice?

Action Step: If you know that you are the type of person to succumb to influencer marketing, or shopping out of boredom, etc, make it somehow more difficult for yourself to just click “buy.” That could be erasing your credit cards from Amazon, it could be putting a sticky note on your phone that says “pause.” However you can create the habit of being more intentional with your spending, do that thing.

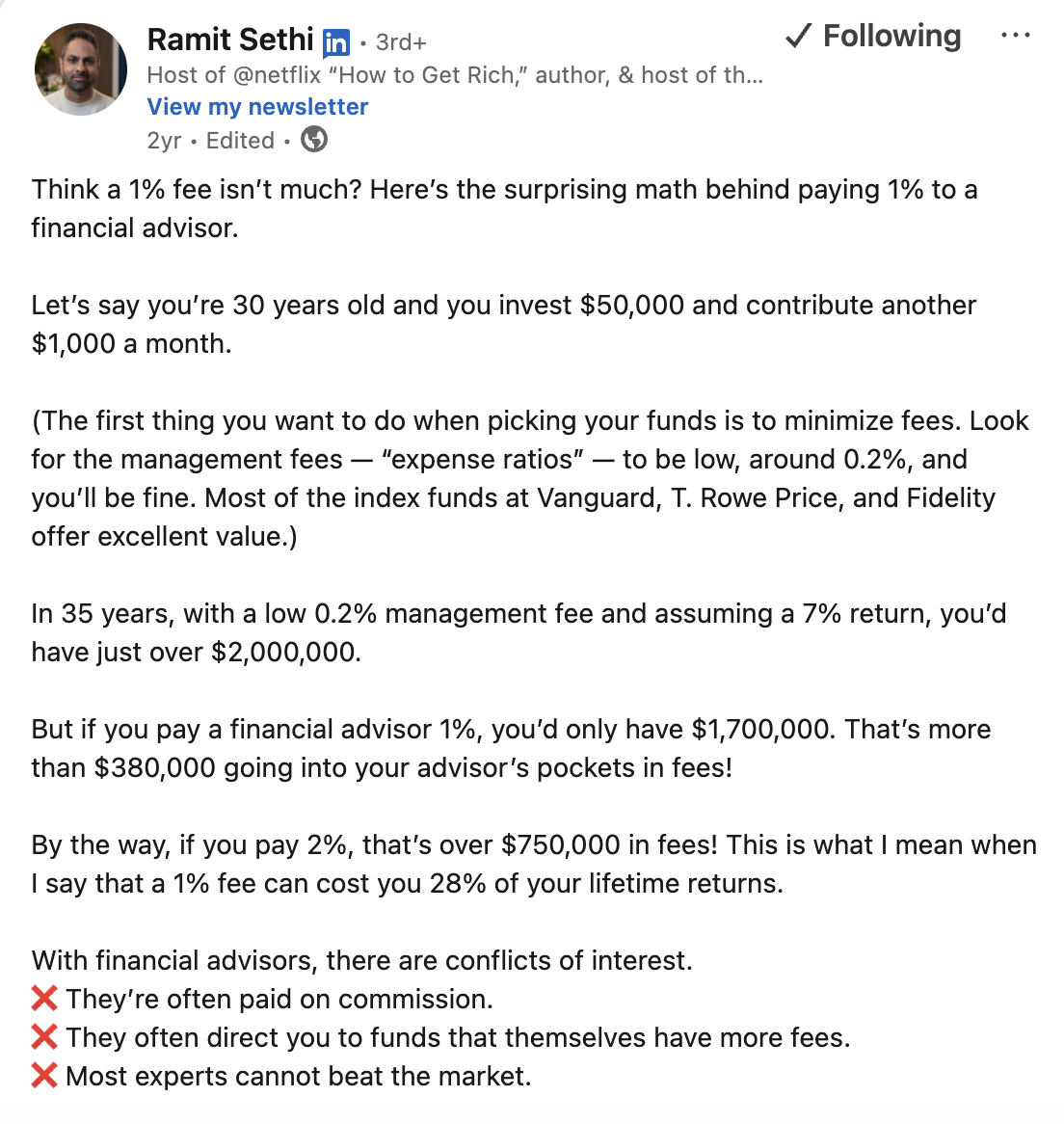

Suggestion 8: Investing is one of the few areas of life where working harder & getting more complicated will hurt you. Science says: If you are a DIY investor and choose broad based, low cost index funds- you will win.

This truth goes against human nature, which is why financial advisors are so profitable. I’m 100% not saying that all financial advisors who charge a percentage of your assets are bad people. I am saying that if you spend one hour learning about how to invest, you will likely beat their returns and keep more of your money.

Here’s Ramit’s take (and all he’s trying to sell you is his $13 book):

Action Step: If you already have a financial advisor, ask how much they are charging- and don’t let them dodge the question. They may say something like, “you’ll never write a check to pay me” or something similarly shady. Ask them what percentage of your assets they are taking as a fee. With the real information, you can make a decision that works for you- as long as you understand the math behind the decision you’re making. (Are they really worth $300k?)

Suggestion 9: “When women and other marginalized groups have money, we get to change the world to be a more equitable, joyful, and safe place.” -Tori Dunlap, Financial Feminist

Oh but I love it when women start talking honestly about money! If you identify as a woman and feel like talking about money isn’t feminine, or leans immoral, or have thought “why should I have money when so many others don’t?” then I highly suggest starting with Tori’s book and/or podcast.

She makes it clear that when women have money, they can do all kinds of amazing things, like leave unhappy/horrible/abusive marriages, quit toxic jobs and give money to those that need it. And it doesn’t take a genius to see that when women have money, they help everyone else. **Gestures widely at the news…

Action Step: If money gives you the ick, ask yourself why that might be. Then ask yourself if what you find is still true for you. If not, that’s a fun new interesting piece of data, no?

Suggestion 10: The average time it takes for someone to become financially independent is 5-15 years, when they take action.

How about them apples? Are you surprised? How old will you be in 5 years? How about 15?

You’ll get to 15 years from now either way (hopefully). Let’s say you are 44, like me. In 15 years you’ll be 59. Would you like to celebrate your 59th birthday with debt, staring down 15 more years of work? Or would you like to celebrate knowing that you have spent the last 15 years purchasing your freedom?

And here’s the thing: you’ll probably get there before 15 years. With focused attention, I’ve never heard of it taking anyone that long.

Action Step: Start dreaming. What does a perfect Tuesday look like for you in retirement? What would you do? Who would you connect with? How would you serve?

PS: This was a lot. I get it. My hope is that you found one or more suggestions that feel right to you. Please let me know in the comments which one you’re taking action on today.

PSS: If you are already in the FI community, let me know- what did I miss?