Nuts & Bolts: Our Withdrawal Strategy

As we draw closer to our official retirement date (29 more weekdays from the day I’m writing this!) the logistics of our withdrawal strategy have obviously been top of mind. One, because we really need to have this ish figured out by now and two, because I find it endlessly interesting.

Financial independence nerds unite!

To that end, I’ve been revisiting some podcasts and bloggers that I’ve found over the years and bookmarked for just this occasion. Three years ago, I didn’t need to worry too much about sequence of returns risk or tax strategies in retirement. Now? Don’t tempt me with a good time!

The aim of this post is to give a high level view of our withdrawal strategy in the hopes that it doesn’t feel so amorphous to those of you working towards financial independence- and honestly, I hope it grounds the strategy a bit more for me too.

Onwards!

The Bucket Strategy

The bucket strategy has been around for a long time, but in the FIRE community (Financial Independence, Retire Early) there is one guy associated with this method of withdrawal- Fritz Gilbert at The Retirement Manifesto.

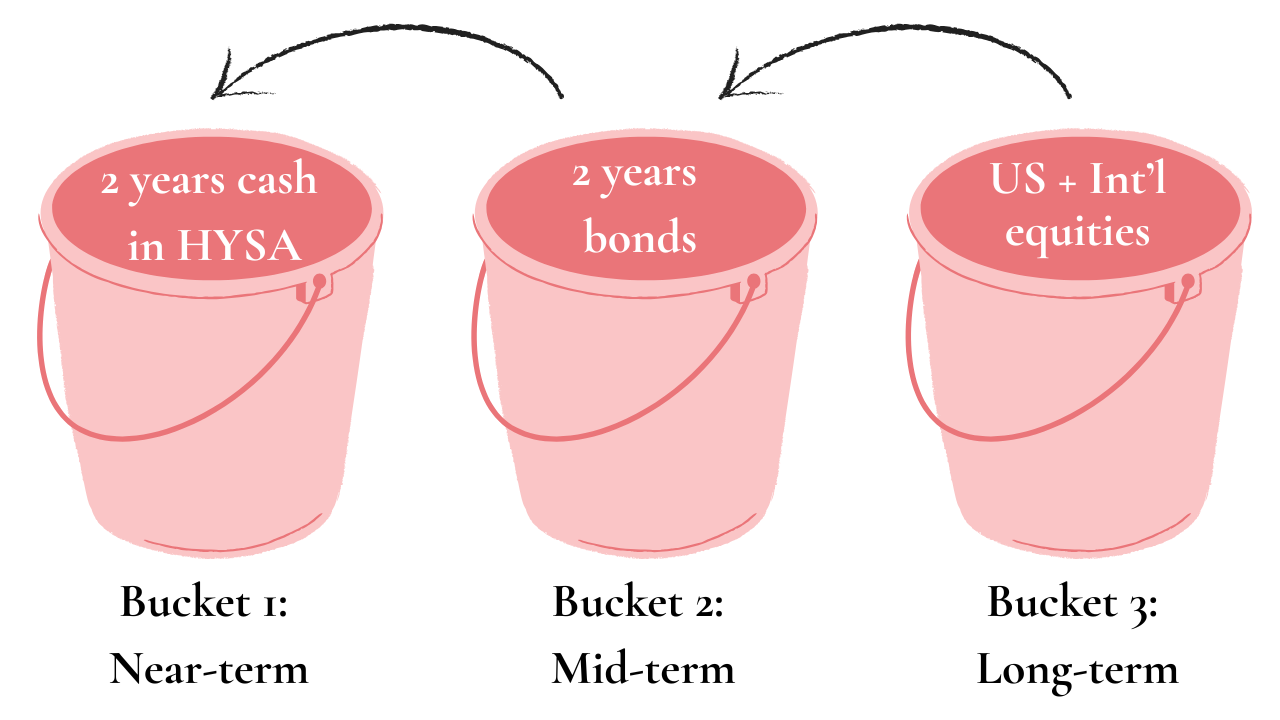

Imagine three big buckets:

Bucket one has 2-3 years worth of spending in assets that are not impacted by the market (so, cash).

Bucket two has 3-8 years worth of spending in low volatility assets, like bonds.

Bucket three is your growth bucket- usually all equities that you won’t need to touch for a long time (or the amount of time that your first two buckets last).

What’s a bit different about our situation is that Ryan’s pension covers 50% of our yearly spend, so we only need to cover the other 50%. However- in the 50% that we need to cover, our spending could be variable if needed. That gives us some built-in safety, or what FIRE folks call “a higher floor.”

For this reason, there is a bit less than the recommended allotments in our first two buckets.

Here’s how our specific buckets look, not including the pension:

Bucket one: 2 years of cash in a high yield savings account.

Bucket two: 2 years of bonds.

Bucket three: equities, split between VTSAX and VTIAX. This portion accounts for ~80% of our portfolio.

Canva for the win!

The bucket strategy appeals to me because I’m a visual learner- even though there are no literal buckets, the portfolio makes more sense to me apportioned out in this way. I also really love how it feels in my body to know that even if the market takes a dive, we have four years of cash and bonds at the ready. Because sleeping well at night? That’s the whole ballgame.

How We Will Draw Down

Starting in June, our first pension check will be automatically deposited into our bank account (yippee!). Because this is only half of our spending needs, we will then create a “paycheck” from our buckets for the other half.

The pension will be deposited around the 25th of each month- so, to mimic our current biweekly paychecks, I’ll schedule an automatic withdrawal from the high yield savings account to deposit into our checking account two weeks prior.

To begin with, we will use a 4% withdrawal rate. This is in line with Bill Bengen’s study and the now infamous “4% rule.” After we get our sea legs under us and start to feel a bit more confident in our strategy, my hope is that we move to use spending guardrails. This will help make our spending more dynamic to follow market fluctuations- because why not spend more when the market is rocking out?

Rebalancing

Our plan is to rebalance our portfolio and refill our buckets once a quarter.

So, if we start drawing down from our cash bucket in June using the method above, by the time we get to Q3 we will have spent three months of cash from that bucket.

We’ll take a look at our portfolio at that time. Here’s what we’ll do in each scenario:

Stocks are up & bonds are down: Sell some stocks to refill bucket number one.

Stocks are down & bonds are up: Sell some bonds to refill bucket number one.

Both are down: Leave everything alone, check again in Q4. (*remember- we have 2 years of cash runway for this eventuality)

Both are up: Rebalance according to our desired asset allocation (2 years cash, 2 years bonds, mucho years equities).

Year End Deep Dive

At the end of the year, we’ll do a deep dive on current net worth, asset allocation and whether or not we need to make any changes. 2026 especially will be a bit of an anomaly as it will be split pretty evenly between earning W2 income and beginning our retirement drawdown journey- a learning experience for sure.

Phew! Still awake? If you’re still in the accumulation phase, (or in the debt paydown phase, or in the “I just want to learn about this stuff” phase) I’d love to know what questions you have. Send me an email or leave your question in the comments below.